Since there is no rule stating that you must use your HSA to directly pay for medical expenses or that you must withdraw money from your HSA within a certain amount of time after paying for a medical expense, you can just take out the money whenever you want.

As long as the qualified medical expense occurred after the HSA was opened, you can withdraw money from the HSA at any time after incurring the expense to reimburse yourself. (View Highlight)

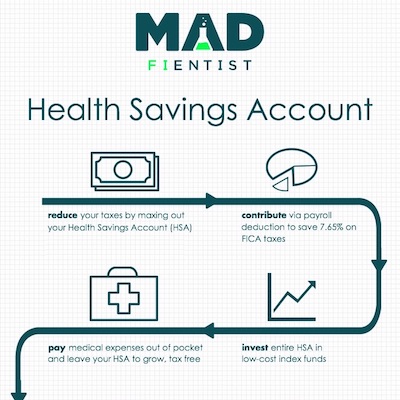

The great benefit of having an HSA is that I can decide when to pay myself back. Since I am already maxing out my other tax-advantaged accounts and have ample savings, a $200 payment isn’t going to break the bank so there’s no rush to get paid back from my HSA. Instead, I am able to leave that $200 in my HSA to grow tax-free until I decide to withdraw it! (View Highlight)

Like a Traditional IRA, your contributions to the HSA are pre-tax contributions and your contributions are allowed to grow tax free. If you don’t use your HSA funds for medical expenses, you can begin withdrawing money from your HSA account for any expenses after you turn 65, without penalty. You’ll have to pay income tax on any distributions that aren’t for qualified medical expenses, just like you would with a Traditional IRA, but you won’t incur any additional penalties or fees.

Therefore, after the age of 65, an HSA is nearly identical to a Traditional IRA but it’s still better because your withdrawals for medical expenses are still completely tax free! (View Highlight)